Understanding the Sarbanes-Oxley (SOX) Act: Key Compliance Insights for Public Companies

Understanding the Sarbanes-Oxley (SOX) Act: Key Compliance Insights for Public Companies to strengthen controls, transparency, and audit readiness.

Accorp Compliance Team

Our team of compliance experts specializes in PCI DSS, SOC 2, and other security frameworks to help businesses achieve and maintain compliance.

The Sarbanes-Oxley Act (SOX) is a landmark piece of U.S. federal legislation passed in 2002 with the goal of restoring investor trust following major corporate accounting scandals, such as the collapse of Enron and WorldCom. The law established significant reforms to improve corporate transparency, hold executives accountable, and prevent fraudulent financial reporting among publicly traded companies.

The legislation lays out specific responsibilities for corporate executives, particularly board members, and enforces stringent rules around financial disclosures and auditing practices. It also introduced criminal penalties for those found guilty of misconduct or deception in financial reporting. Oversight of SOX implementation is carried out by the Securities and Exchange Commission (SEC), which issues regulations and guidance for public companies to follow.

Spotlight on Section 404: Internal Control Reporting

Among the many provisions in SOX, Section 404 is one of the most talked about—especially when it comes to compliance. This section requires that a public company’s annual financial filings include an Internal Control Report, where management must affirm the existence of an effective internal control structure over financial reporting.

Furthermore, management must provide a self-assessment of those controls, and an independent auditor must validate this assessment. If there are control deficiencies or gaps, they must be identified and disclosed. The objective is to ensure that internal accounting practices are not only documented but are actually functioning as intended.

PCAOB Guidance and Auditing Standards

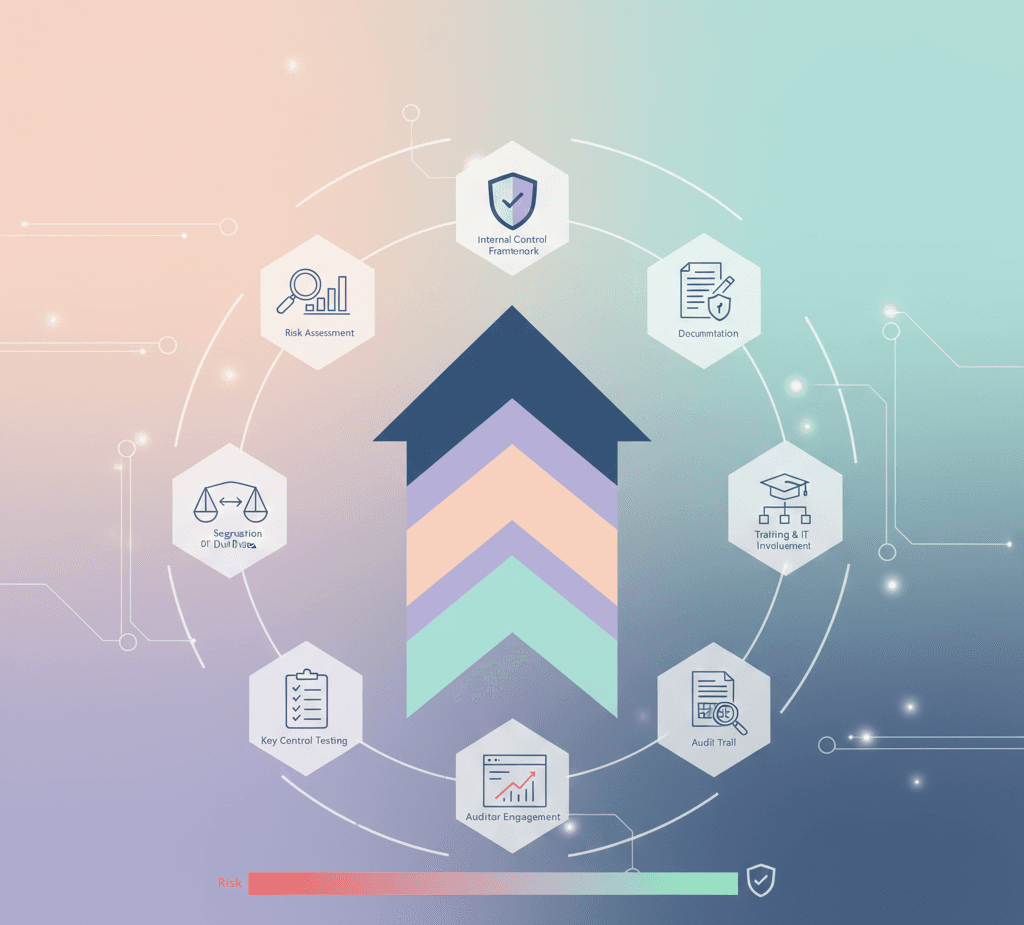

To support compliance with SOX, the Public Company Accounting Oversight Board (PCAOB) introduced Auditing Standard No. 5 (AS5) in 2007, which replaced the earlier AS2. AS5 clarified how both management and auditors should approach the internal control assessment using a risk-based, top-down methodology. This approach helps companies focus on areas where financial misstatements are most likely to occur.

Key responsibilities outlined by AS5 include:

Mapping the flow of financial data to identify potential points of error or fraud.

Performing a fraud risk assessment over the financial reporting process.

Testing controls tied to relevant financial assertions to assess their design and operational effectiveness.

Evaluating organisation-level controls using the COSO framework as a benchmark.

Identifying both preventive and detective fraud controls.

Concluding whether the internal controls are adequate, and documenting any weaknesses that need remediation.

Since AS5, other auditing standards have been introduced to guide audit professionals on topics like auditor independence, documentation practices, audit risk, and evidence collection. These evolving standards ensure that audits are thorough, consistent, and aligned with regulatory expectations.

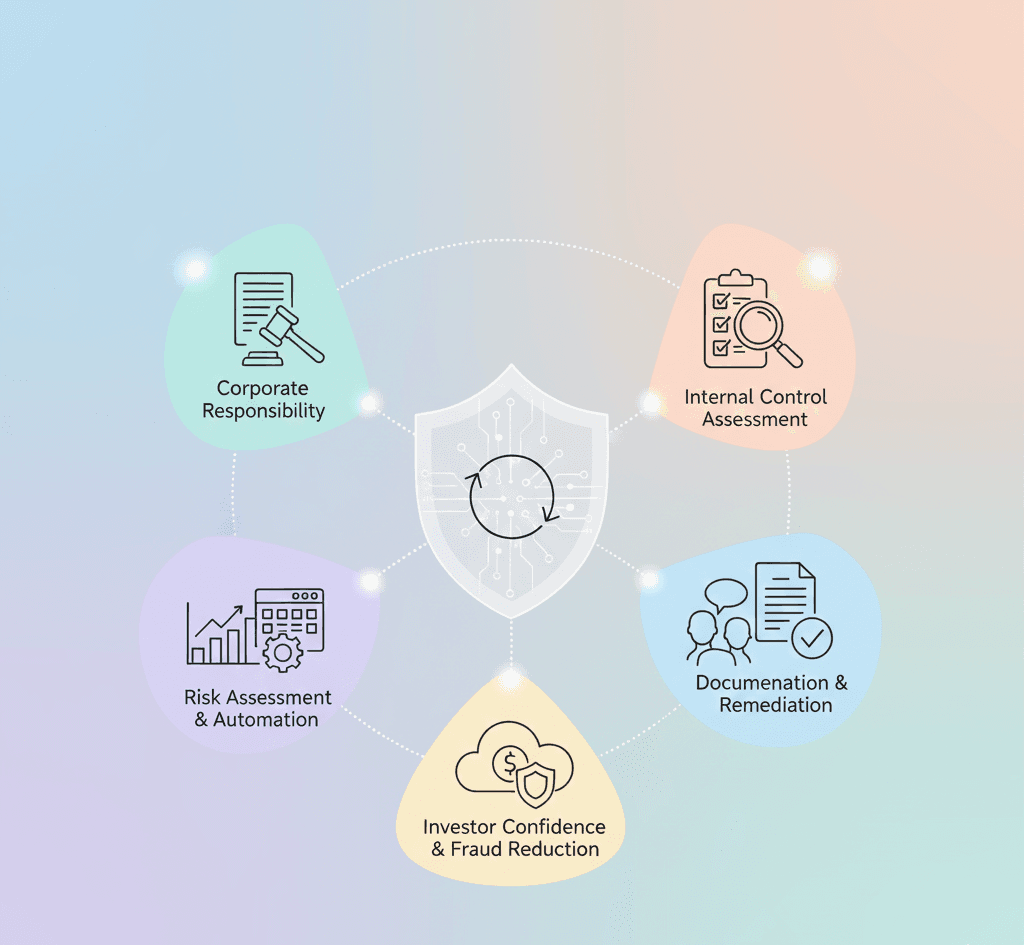

Who Benefits from SOX Compliance?

While SOX compliance can be demanding—especially for small- and medium-sized public firms—it has also raised the bar for corporate accountability. One clear benefit is the increase in investor confidence due to improved reliability of financial statements. However, some critics argue that the cost and complexity of compliance can outweigh the perceived benefits, particularly for smaller organizations.

In response, many companies now rely on compliance automation software to streamline internal control testing, reporting, and auditor communication. These tools, often part of the growing SaaS ecosystem, help reduce time and costs associated with SOX-related documentation.

Final Thoughts: The Role of SOX in Corporate Governance

SOX has significantly reshaped the governance landscape by requiring transparency and stronger internal controls from public companies. By mandating annual internal control assessments, certified by external auditors, and enforcing accountability at the management level, the law helps reduce the risk of corporate fraud and financial misstatements.

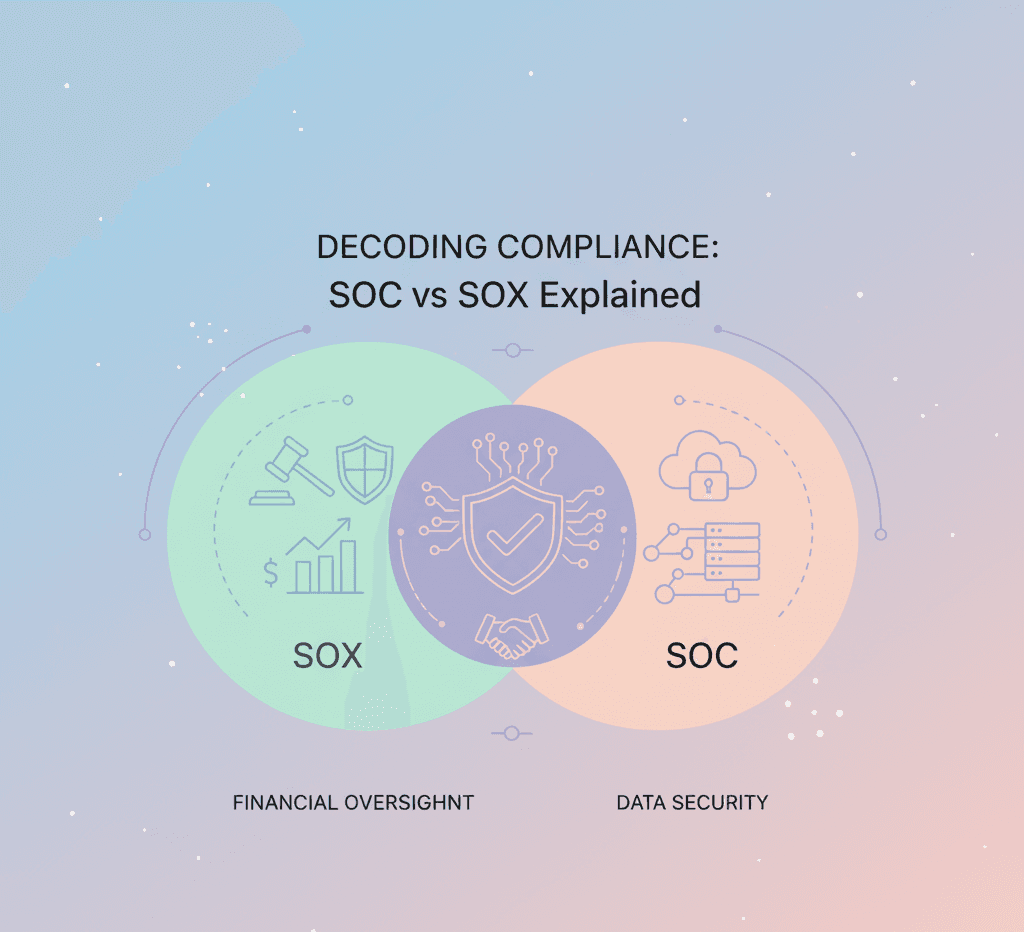

Although Accorp does not provide SOX-specific audit services, our deep expertise in risk and compliance frameworks—including SOC 1 & SOC 2, HIPAA, ISO 27001, and FedRAMP—positions us to assist clients in developing strong, audit-ready control environments. Whether you’re preparing for regulatory review or enhancing your cybersecurity posture, we’re here to help you navigate the complexities of compliance with confidence.