Decoding Compliance: SOC vs SOX Explained

SOC vs SOX: Key Differences Explained for Effective sox 404 assessment & Compliance

Accorp Compliance Team

Our team of compliance experts specializes in PCI DSS, SOC 2, and other security frameworks to help businesses achieve and maintain compliance.

In the world of financial reporting and data security, SOC and SOX compliance are two essential frameworks that strengthen internal controls, boost operational trust, and protect both investors and customers. While they serve similar goals, these compliance measures are fundamentally different in scope, application, and legal obligation. Understanding these differences is crucial for ensuring your business follows the right standards and meets SOX compliance requirements where needed.

Let’s explore SOC vs SOX, key distinctions like SOX 404 requirements, and how these frameworks align with risk and control strategies, such as the SOX 404 assessment and SOX risk assessment.

What is SOX Compliance?

The Sarbanes-Oxley Act (SOX), passed in 2002, is a U.S. federal law introduced in response to corporate scandals involving companies like Enron and WorldCom. It was created to protect investors by improving the accuracy and reliability of corporate disclosures.

SOX is mandatory for all publicly traded companies in the U.S. and any foreign entities with U.S. operations. It imposes strict regulations on financial reporting, internal controls, and corporate governance—covering everything from internal audits to SOX 404 internal audit readiness.

Key SOX Compliance Requirements:

Section 302: Executive responsibility for financial reports

Section 404: Requires management to establish, maintain, and report on internal controls over financial reporting (ICFR)

Section 409: Real-time disclosure of material changes

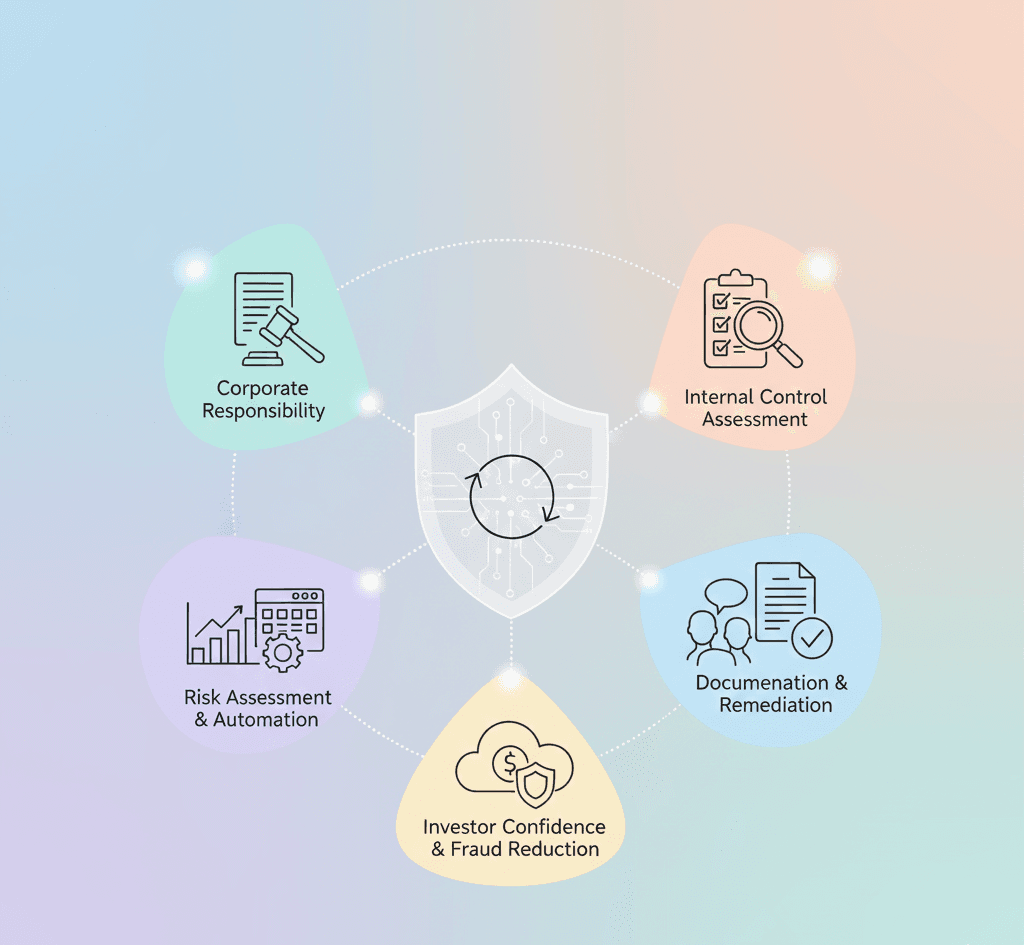

The most critical among these is SOX 404, which demands that organisations not only implement internal controls but also have them independently audited each year. This includes detailed documentation, testing, and effectiveness validation—often part of both SOX 404 assessment and SOX 404 risk assessment workflows.

Benefits of SOX Compliance:

Strengthens financial transparency

Reduces risk of fraud and data breaches

Builds investor trust

Enhances governance and accountability

As part of SOX 404 requirements, businesses must assess their internal control environment, test control performance, and ensure continuous compliance readiness—whether through SOX type 2 audits or external attestations.

What is SOC Compliance?

SOC stands for System and Organisation Controls. It is a framework developed by the American Institute of Certified Public Accountants (AICPA) to help service organisations demonstrate that they have proper controls in place to protect client data and systems.

Types of SOC Reports:

SOC 1: Focuses on internal controls relevant to financial reporting (ICFR) – especially useful for companies servicing SOX-compliant clients.

SOC 2: Evaluates data handling against AICPA’s Trust Services Criteria – security, availability, processing integrity, confidentiality, and privacy.

SOC 3: A public-facing version of SOC 2, meant for general distribution.

SOC compliance is not legally mandated, but it’s a competitive necessity for SaaS providers, cloud platforms, and data processors. These reports often include IT general controls testing — a critical component for technology-driven organisations.

Benefits of SOC Compliance:

Demonstrates strong data security and privacy controls

Helps service providers support their clients’ SOX compliance requirements

Builds trust with customers and partners

Reduces exposure to cyber threats and compliance risks

Key Differences Between SOC and SOX

Feature | SOX Compliance | SOC Compliance |

Mandated By | U.S. Federal Law | AICPA (voluntary) |

Applies To | Public companies | Service organizations |

Focus | Financial reporting accuracy and internal control design | Operational & data security controls |

Audit Frequency | Annual (mandatory) | As required/requested |

Audit Scope | Covers ICFR, governance, and disclosures | Covers security, privacy, and system availability |

While SOX 404 internal audit focuses on ensuring robust financial control systems, SOC 2 is more aligned with information security and IT infrastructure evaluations—making them both valuable but different in application.

How SOX and SOC Relate to MAR

Many insurers must also comply with MAR (Model Audit Rule), which is based on SOX 404 requirements. MAR applies SOX-like standards to the insurance industry, mandating internal control assessments and annual financial audits.

As part of internal control design SOX MAR compliance, insurers must evaluate internal controls, document procedures, and submit independent audit reports—much like the SOX risk assessment process. MAR aligns closely with SOX type 2 reporting around operational effectiveness.

Why Accorp?

At Accorp, we help organisations prepare and maintain compliance across SOX, SOC, and MAR standards. Our expertise includes:

SOX 404 assessment and documentation

Comprehensive SOX risk assessment frameworks

IT general controls testing for SOC 2 readiness

MAR compliance services for insurers

Whether you’re preparing for a public audit or building customer trust through data security practices, we offer tailored compliance solutions to meet your regulatory needs.

Conclusion

SOC and SOX compliance may seem similar, but they serve different regulatory and operational needs. Understanding whether your business needs SOX 404 compliance, SOC reports, or MAR compliance is key to staying ahead of legal and market expectations. By aligning your controls with both SOX 404 requirements and SOC criteria, you build a robust, trustworthy business foundation.