When Should SOC 1 Reports Be Considered

Learn when a SOC 1 report for service organisations is needed, how it impacts financial reporting, and why it matters for audit assurance.

Accorp Compliance Team

Our team of compliance experts specializes in PCI DSS, SOC 2, and other security frameworks to help businesses achieve and maintain compliance.

A common question we hear from both current and potential clients is: “What exactly is a SOC 1 report, and when does it apply?” Our answer usually comes back as another question: “Do your services have an effect on your clients’ financial reporting?”

Sometimes the response is immediate — the client describes a process that clearly impacts financial statements. Other times, the answer is less direct. For instance, a company may only have read-only access to client data without the ability to alter or influence financial records. In those cases, their services (such as providing reporting tools or analytics dashboards) don’t directly affect client financials and therefore may not fall under SOC 1 scope.

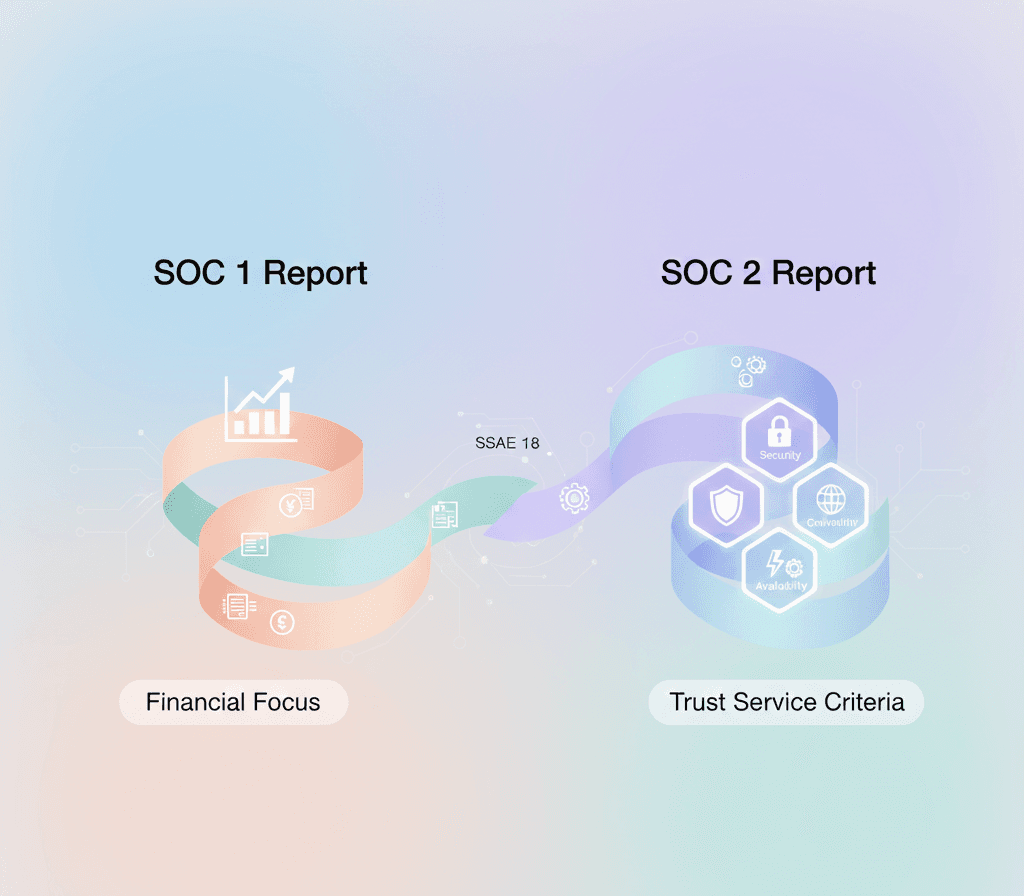

What Is a SOC 1 Audit Report?

A SOC 1 is an attestation report that focuses on both business process controls and IT-related control objectives. These reports must be issued by a licensed CPA firm with expertise in auditing security and process controls.

In practice, management first asserts that specific controls exist to meet stated control objectives. The CPA firm then tests those controls and issues an opinion on whether management’s assertions hold up. Unlike SOC 2 reports, which follow a set of predefined Trust Services Criteria, SOC 1 reports are customized to the service organization and the processes under review.

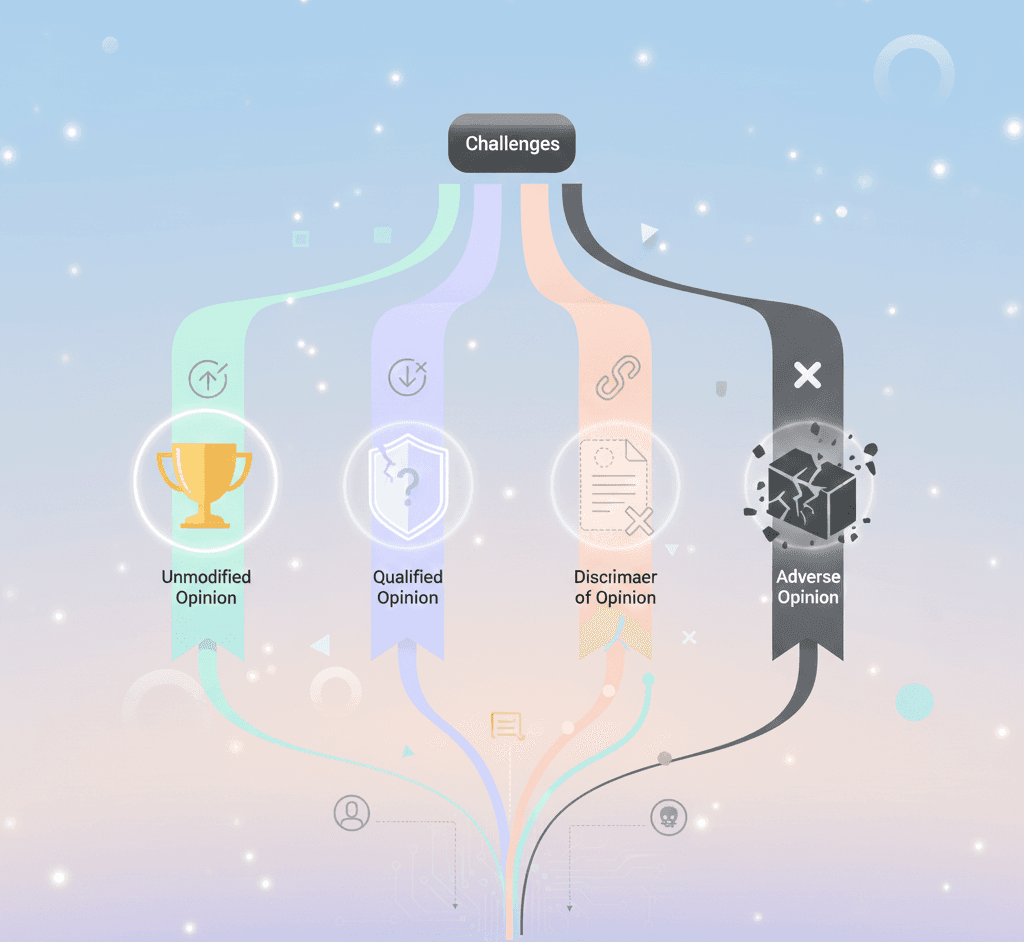

The auditor’s opinion can be either unqualified or qualified (noting exceptions). If qualified, the opinion letter will highlight which objectives weren’t fully met.

Understanding Control Objectives and Their Role

Control objectives are the high-level goals that controls are designed to achieve within each SOC 1 process area. They describe the risks being addressed and the expected outcome.

For example, one control objective might state:

“Controls provide reasonable assurance that access to systems, programs, and data relevant to financial reporting is limited to authorized users who perform only approved actions.”

Once objectives are defined, management and the auditor work together to identify specific controls that support them. These could include things like password policies, multi-factor authentication, role-based access restrictions, and physical security measures.

It’s important to note the phrase “reasonable assurance.” The auditor’s role is not to guarantee perfection. Instead, the objective is to determine whether there are enough effective controls in place to reasonably conclude that the risk is managed, even if one or two individual controls fail.

In a SOC 1 Type II report, the auditor must confirm that controls were both designed properly and operated effectively throughout the reporting period.

Why SOC 1 Reports Matter

SOC 1 reports are especially valuable for external financial auditors. If a client outsources part of their financial processes, the auditor can rely on the SOC 1 report instead of re-performing audit procedures over the service organization. This allows for efficient, reliable audits while still addressing outsourced risks.

What is a Service Organization?

The AICPA uses the term service organization to describe companies that provide outsourced services impacting their clients’ operations. When those outsourced services affect financial reporting, SOC 1 becomes relevant.

Take payroll as an example. A company like ADP manages payroll for thousands of businesses. Because payroll directly impacts financial statements, ADP is considered a service organization whose processes must be audited under SOC 1. Errors or gaps in their controls — whether accidental or intentional — could materially impact client financials, which is why a SOC 1 report is often required.

In short, SOC 1 applies to service providers whose activities could have a direct effect on the financial reporting of their clients.